--- the subscriber area has no ads and those above are not selected or endorsed by this site ---

inflation, and macro implications +1

14:56 15-Mar-22

Here's a macro freebie where the links and analysis last paragraph may also be helpful for EV buyers...

On 3/15/22 14:05, Esekla wrote:

The Westport conference call has concluded. The main thing I want to add is management's update on China, where HPDI 2.0 field trials with LNG are ongoing, and current LNG prices are a headwind. This underscores the view I've taken, which anticipated the current bump in demand, but also the destruction of it due to the supply gap that I think will power producers like New Fortress and Golar....

To put some numbers on relative commodity volatility that I mentioned yesterday, Brent has dropped over 30% from its peak a week ago to trade right around $100 this morning, with WTI now over $4 below that. Yet Henry Hub gas is only about 10% lower than the price cited there, right back in the middle of the $4-5 range where New Fortress and I think it should be. TTF & JKM are priced in the mid & low $30s through the fall, respectively, though it is notable that JKM is currently back to outbidding TTF for April. I continue to predict that the disparity in volatility will help support the world's move toward natural gas and better stewardship of its climate. In further support of the geopolitical and commodity progression I've foreseen, the Saudis are reportedly in talks to price oil sales in yuan and Schlumberger has announced a major (but unquantified) gas development project with them. Three Eastern E.U. leaders are also forgoing western leadership and safety and visiting Kyiv in person to meet with Zelensky, even as Putin continues shelling it. Although none of this is likely to affect short term stock prices, this is me pounding the table on NFE and KNTK for the medium term, and BGCP for the long term.

To understand why, consider this morning's Producer Price Index print for February which showed continued 10% YoY inflation. Yet this is being hailed as moderation because the monthly 0.8% and 0.2% excluding food & energy numbers were below 1.0% and 0.6% expectations. Recall that Russia invaded Ukraine on February 24th, then look at the Fed's own 1-year graph, and let me know whether or not you are relieved:

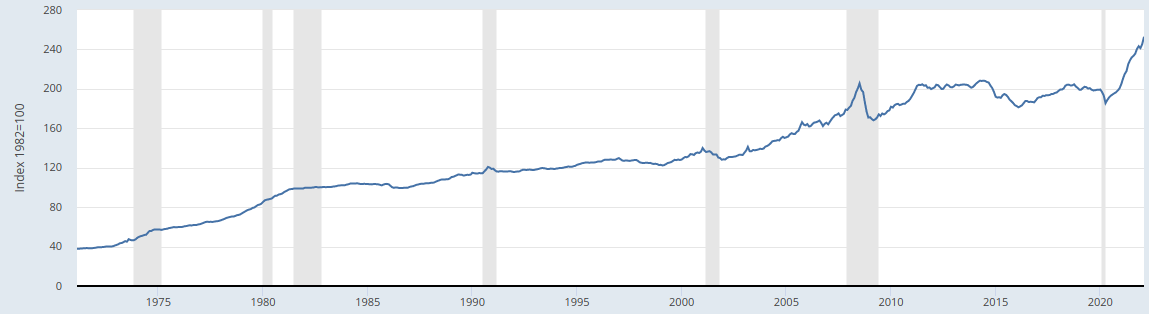

To see what this means for the market and economy, here's PPI over the entire modern era:

which I define as the period since Nixon switched the world to fiat currency. In my opinion, any comparison preceding that event is moot. The shaded areas indicate recessions, and what I see beyond the obvious correlation is increased duration and/or severity, which I attribute to the rise of electronic trading, options and leverage in the market, and debt in the economy. Of course, you can tune into any financial news media distributor to find some pundits talking their books, and saying this time will be different. I agree, but not in a good way. My opinion is that utilities and natural gas producers will come through this just fine, overcrowded index-dominating mega-caps and the consumer discretionary products being supported by Magnachip's latest market entry, not so much.

Tesla just had to raise prices across its entire product line, further indicating that Polestar and other newer entrants will be (unfairly, IMO) advantaged by federal tax credits, which are unlikely to change anytime soon, per the appropriations notes also provided last night. Hopefully readers can forgive my at least momentary reluctance to write that it seems Putin might be killing Ukrainians with China's at least tacit support mainly to de-weaponize America's currency, which is why I continue cite BGCP for the long term. Hopefully, they also now understand why I'll be much more interested in the status of Xebec's new American manufacturing for renewable natural gas on Thursday than in the details surrounding the Fed's quarter point hike tomorrow.